Summer Sale – Grab discounts on some of our hottest conference destinations, credit packages & Tax Updates

Leslie Book, Professor of Law, Villanova University School of Law, Principal Author, Saltzman and Book, IRS Practice and Procedure

As originally appearing in Procedurally Taxing on August 19, 2022.

In a major decision that considers the implications of last year’s CIC Services opinion, the First Circuit in Harper v Rettig has held that the Anti-Injunction Act (AIA) does not bar a constitutional challenge to the IRS’s use of its John Doe Summons authority that allowed it to obtain information about a taxpayer’s virtual currency transactions.

The IRS has been actively using its John Doe summons powers to get taxpayer information from virtual currency exchanges. One of those cases involved a summons on Coinbase as part of an investigation into the reporting gap between the number of virtual currency users Coinbase claimed to have and the number of U.S. bitcoin users reporting gains or losses to the IRS during 2013 through 2015.

After Coinbase refused to comply, the government moved to enforce the summons. Following a skirmish about the scope of that summons, and a district court’s decision to allow a third party to intervene under Federal Rule of Civil Procedure 24, the court issued an order enforcing the summons. I discussed some of the procedural skirmishes a few years back in A PT Anniversary and Court Finds IRS Summons on Coinbase Suggests an Abuse of Process.

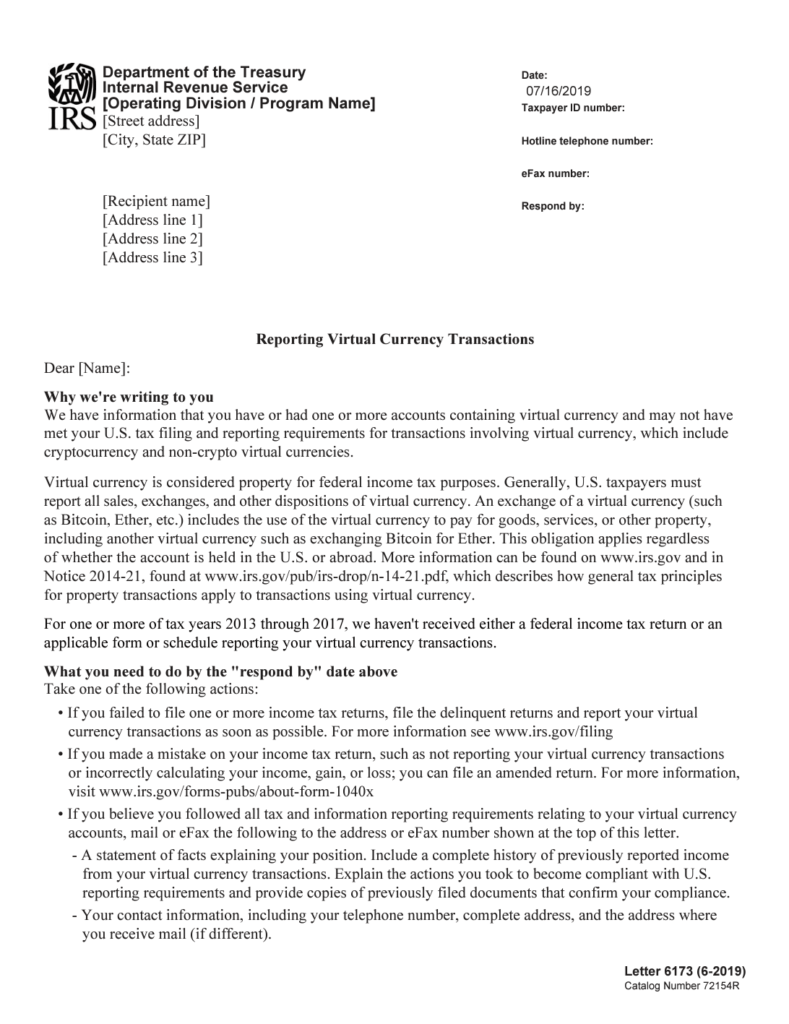

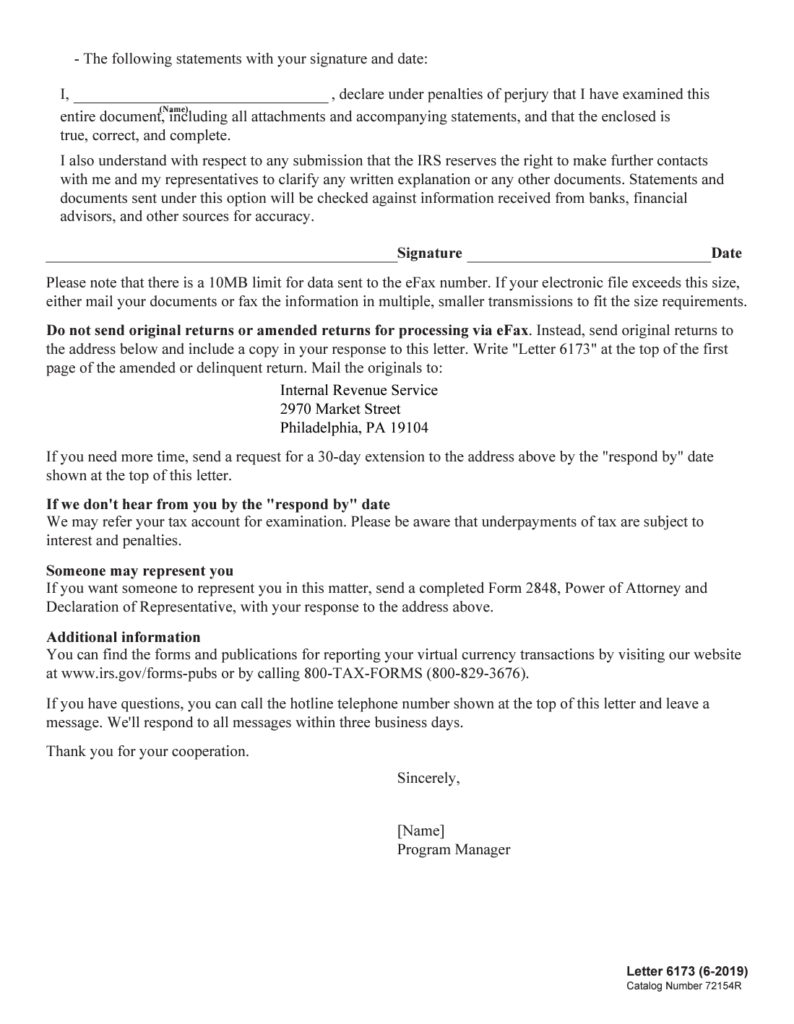

Fast forward a few years, the IRS has been using the information it received to contact taxpayers it believes have failed to properly report their income from the virtual currency transactions. One of those taxpayers was James Harper. The IRS sent Harper a letter that informed him of the requirements for reporting virtual currency transactions. It helpfully told him if he believed he had not accurately reported such transactions, he should file amended or delinquent returns. The letter also warned that if he had not “accurately report[ed his] virtual currency transactions,” then he “may be subject to future civil and criminal enforcement activity.”

10,000 virtual currency owners received an educational letter three variations: Letter 6173, Letter 6174 or Letter 6174-A

The three letters, sent by the IRS, was intended to help taxpayers understand their tax and filing obligations and how to correct past errors.

Shortly after receiving the letter Harper filed suit in a federal district court in New Hampshire. One aspect of the suit involved a request for injunctive and declaratory relief, alleging that the IRS unlawfully obtained his financial information from virtual currency exchanges in violation of the Fourth and Fifth Amendments.

The District Court held that the Anti-Injunction Act (AIA) deprived the court of subject matter jurisdiction over the taxpayer’s claims for injunctive and declaratory relief.

Harper appealed and claimed that the AIA did not bar his suit because his suit pertained to the information gathering function of IRS activity, rather than the assessment or collection process.

The government and district court distinguished CIC Services, noting that in that case the plaintiff sought to avoid the economic burdens of providing information about other taxpayers to the IRS and challenged its legal obligation to do so. According the government, and unlike in CIC Services, Harper “simply does not want the IRS to possess information bearing on his tax liability.”

Back when the Supreme Court issued its opinion in CIC Services PT had many posts that discussed the uncertain boundaries of that opinion, and whether courts may apply it more broadly than the circumstances of that challenge. See for example Bryan Camp in Supreme Court Reverses the Sixth Circuit in CIC Services – Viewpoint and my post Further Initial Thoughts on CIC Services.

In a relatively brief opinion, the First Circuit reversed, finding that CIC Services and the earlier Direct Marketing opinion opened the door to Mr. Harper’s challenge because the summons authority and IRS activities to enforce the summons “clearly fall with in the category of information gathering, which the Supreme Court has distinguished from acts of assessment and collection.” As such, the court held that Harper’s suit “challenges the IRS’s information-gathering authority and the Anti-Injunction Act limits our jurisdiction only in suits involving assessment and collection.”

The First Circuit disagreed:

As the Court observed in CIC Services, however, “[t]he Anti-Injunction Act kicks in when the target of a requested injunction is a tax obligation — or stated in the Act’s language, when that injunction runs against the ‘collection or assessment of [a] tax.'” Id. at 1590. Here, the target of the requested injunction is the IRS’s continued retention of appellant’s personal financial information, which appellant alleges the IRS acquired in violation of the Constitution and 26 U.S.C. §7609(f)

Drilling even deeper into the nature and purpose of the AIA vis a vis the relief Harper sought, the court viewed his suit as not attempting to limit the IRS’s ability to redetermine his tax:

Contrary to the IRS’s suggestion that appellant’s suit is “a ‘preemptive’ suit to foreclose tax liability” (which would be barred by the Anti-Injunction Act), this suit, like the suit at issue in CIC Services, “falls outside the Anti-Injunction Act because the injunction it requests does not run against a tax at all.” Rather, “[t]he suit contests, and seeks relief from, a separate legal” wrong — the allegedly unlawful acquisition and retention of appellant’s financial records. Like the plaintiff in CIC Services, appellant “stands nowhere near the cusp of tax liability,” and “the dispute is [not] about a tax rule,” where “the sole recourse” in light of the Anti-Injunction Act “is to pay the tax and seek a refund…”

This case is remanded back to the district court to consider whether Harper has stated a claim on which relief can be granted. That is an uphill battle. The IRS appears to have lawfully obtained the information through the summons process, but this interim victory is important as it reflects at least one circuit’s view that courts are to liberally apply CIC Services and not limit it to situations when third parties are challenging IRS’s information reporting obligations.

Subscribe to our news, analysis, and updates to receive 10% off your first purchase of an on-demand digital CPE course.