Summer Sale – Grab discounts on some of our hottest conference destinations, credit packages & Tax Updates

The AICPA Accounting and Review Services Committee recently issued Statement on Standards for Accounting and Review Services (SSARS) 25, Materiality in a Review of Financial Statements and Adverse Conclusions, effective for engagements performed in accordance with SSARS for periods ending on or after December 15, 2021. Early adoption was permitted.

Let’s start with a summary of the revisions and conclude with some pro-tips to assist with your Review Engagements.

The revisions include:

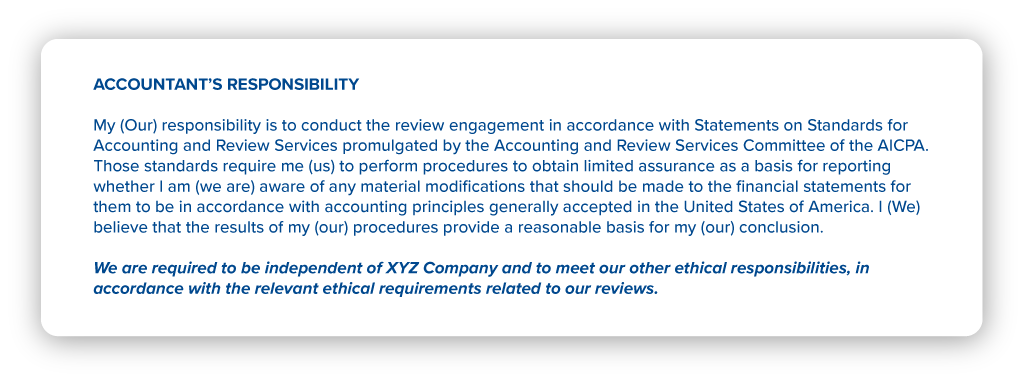

Illustration of change to the Review Report for the requirement of the Independence Statement per SSARS 25 (Page 85-86):

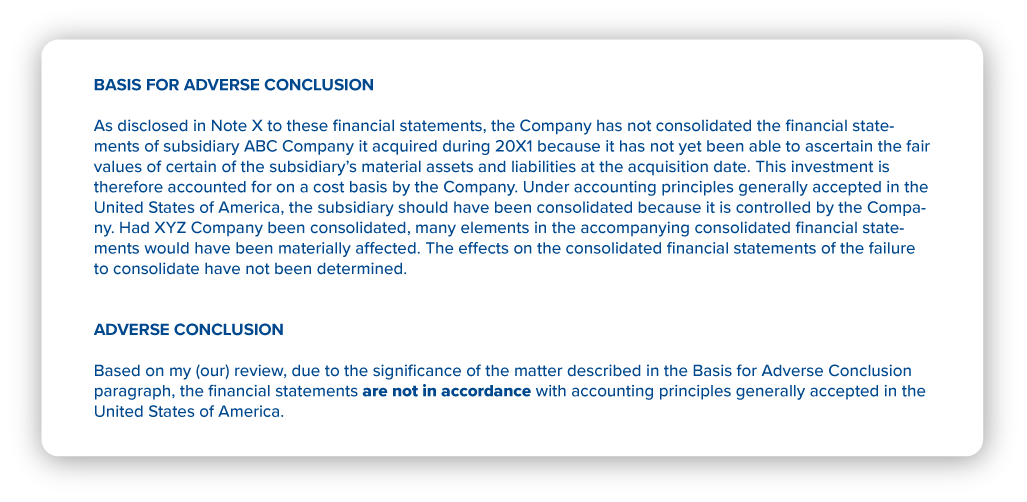

Illustration of Adverse Conclusion in the Review Report as allowed per SSARS 25 (Page 86):

Discover all of Sunish Mehta’s latest CPE courses. With over 25 years of experience and an engaging teaching style, you can’t go wrong.

Subscribe to our news, analysis, and updates to receive 10% off your first purchase of an on-demand digital CPE course.

By:

By: